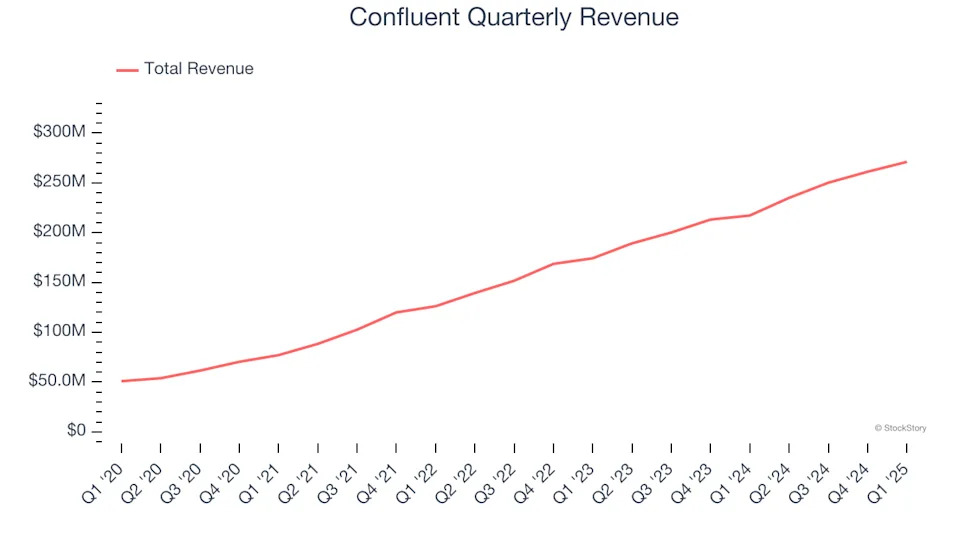

Data infrastructure software company, Confluent (NASDAQ:CFLT) reported Q1 CY2025 results topping the market’s revenue expectations , with sales up 24.8% year on year to $271.1 million. On the other hand, next quarter’s revenue guidance of $267.5 million was less impressive, coming in 3.9% below analysts’ estimates. Its non-GAAP profit of $0.08 per share was 18.3% above analysts’ consensus estimates.

Is now the time to buy Confluent? Find out in our full research report .

Confluent (CFLT) Q1 CY2025 Highlights:

“Confluent started the year with solid momentum, achieving subscription revenue growth of 26% year over year,” said Jay Kreps, co-founder and CEO, Confluent.

Company Overview

Started in 2014 by the team of engineers at LinkedIn who originally built it as an internal tool, Confluent (NASDAQ:CFLT) provides infrastructure software for organizations that makes it easy and fast to collect and move large amounts of data between different systems.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, Confluent grew its sales at an excellent 32.5% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

This quarter, Confluent reported robust year-on-year revenue growth of 24.8%, and its $271.1 million of revenue topped Wall Street estimates by 2.6%. Company management is currently guiding for a 13.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 19.8% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and implies the market sees success for its products and services.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

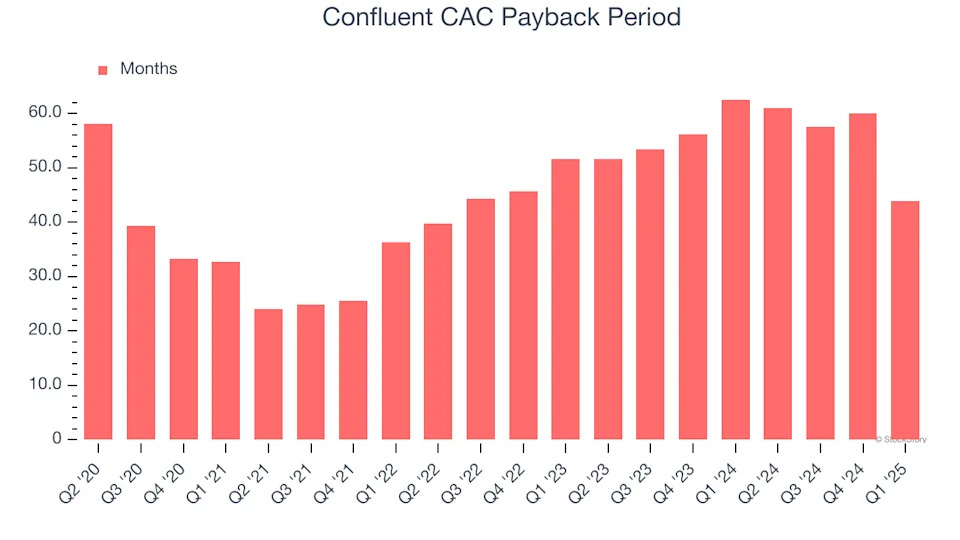

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Confluent does a decent job acquiring new customers, and its CAC payback period checked in at 43.9 months this quarter. The company’s relatively fast recovery of its customer acquisition costs gives it the option to accelerate growth by increasing its sales and marketing investments.

Key Takeaways from Confluent’s Q1 Results

We were impressed by Confluent’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. On the other hand, its full-year revenue guidance missed significantly and its revenue guidance for next quarter fell short of Wall Street’s estimates. Zooming out, we think the weak guidance will weight on shares. The stock traded down 11.2% to $21.10 immediately after reporting.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .